TYPES OF TRUSTS — There are a number of different types of trusts. Some of the more common trusts along with the important aspects and features of each are discussed below.

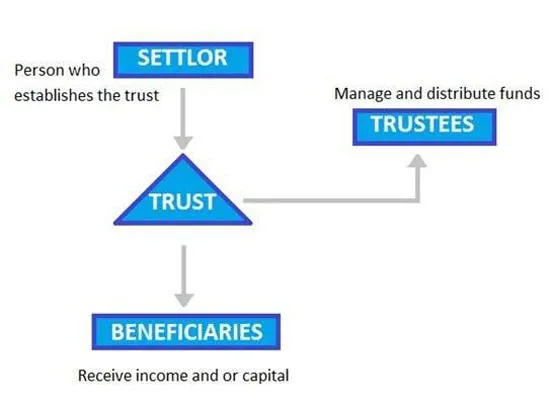

The Settlor of a trust is a person who creates the trust and then transfers property to the trustee who administers and disposes of the trust property on behalf of the beneficiaries, in accordance with the terms of trust agreement. The Trustee is the person who receives the trust property and has the obligation to administer and dispose of the trust property on behalf of the beneficiary of the trust. The Beneficiary refers to a person (or persons) who receive the distribution of trust income from the trustee. The beneficiary can be the same as the settlor of the trust or it can be another person. The beneficiary does not even need to be an existing person as a trust caretaker can be appointed to protect the interests of the future beneficiary.

Asset Protection—The purpose of an asset protection trust is to protect existing assets from a future creditor's attack. The key term is "future creditors" as a trust cannot be set up to protect assets from existing creditors. Asset protection trusts normally are created to be irrevocable for a certain number of years and structured in such a way that the Settlor is not a beneficiary during that period. After the end of this period, the assets of the trust are returned to the Settlor, provided that there is no longer any significant risk of attacks by creditors.

Charitable Trusts—Charitable trusts are established to benefit a particular charitable organization. Most charitable trusts are created as part of a larger estate plan to help lower or avoid certain estate and gift taxes. There are a number of different types of charitable trusts. One of the most common being the charitable remainder trust (CRT) which is often funded with tax-encumbered "income in respect of a decedent" (IRD) assets, such as IRA and 401(k) plans, thus helping to reduce the significant tax burdens of these retirement assets while providing a benefit to charity.

Special Needs Trust—A special needs trust is established to allow a person who receives government benefits due to a disability to qualify for certain "means tested" government benefits. Special Needs Trusts are permitted under the Social Security rules, but they must be set up in such a way that the disabled beneficiary cannot control the amount or the frequency of trust distributions. A Special Needs Trust allows a disabled person who is receiving government benefits to receive an inheritance or a gift without losing their eligibility for those benefits.

Estate Tax Trusts—There are a number of different trusts that can be used to reduce the income tax burden of an estate. One of the most common is the by-pass trust, which allows one spouse to leave money to the other spouse, while reducing the liability of the federal estate tax upon the death of the second spouse. Without a by-pass trust, the assets would pass to a spouse tax-free at the death of the first spouse, but when the surviving spouse dies, any assets over and above the federal estate tax exemption limit still would be taxable. A by-pass trust avoids this problem and can help reduce the federal estate tax burden by a significant amount.